Last year, more than 250,000 students in 17 states used tax-credit scholarships to attend schools their families chose. Under such policies, taxpayers can receive tax credits worth between 50 percent to 100 percent of their donations to nonprofit scholarship organizations that help low- and middle-income students attend private schools.

Because such policies are growing in size and popularity, opponents of educational choice have resorted to “creative” accounting and incendiary rhetoric to discourage policymakers from adopting similar tax credits. They want the public to believe that charitable giving to benefit K-12 students helps donors more than it should; however, their claims do not withstand scrutiny.

Last month, the School Superintendents Association (AASA) and the Institute on Taxation and Economic Policy (ITEP) released “Public Loss, Private Gain,” a report focused solely on condemning tax-credit scholarship (TCS) policies, which they erroneously claim are “far beyond” the tax benefits “available for other charitable donations.” In fact, policymakers have enacted hundreds of tax credits at the state and federal level to incentivize charitable giving intended to aid low-income families, promote innovation, build stronger communities, or benefit the public in other ways. Tax-credit scholarships for K-12 education are just one example, but they are the sole focus of this report.

In addition to the usual talking points—such as lemon-picking research on school choice or warning about constitutional questions that have been long settled in favor of choice—the report alleges that tax-credit scholarship policies “drain public coffers” and “enable savvy taxpayers to turn a profit.” In reality, their allegations of “profiteering” are overwrought, and research clearly shows that TCS policies produce net savings for states. The report also overlooks what matters most: These scholarships are awarded to students who need greater access to educational opportunity.

The Profiteering Canard

One of the central claims in the AASA/ITEP report is that donors somehow profit from their donation. However, beneath the rhetorically charged terms such as “get-rich scheme,” “double-dipping, “tax shelter,” and “tax loophole,” is a rather boring reality: under certain conditions, some taxpayers subject to the Alternative Minimum Tax can reduce their federal tax liability by a larger amount if they make a charitable donation rather than paying their state taxes.

This is not limited solely to donations made to support K-12 education, and it’s not a “profit,” as they would have the public believe. It’s merely a reduction in a taxpayer’s tax liability beyond what the authors of the report believe the taxpayer should have paid.

Here’s how it works: Under tax-credit scholarships programs, taxpayers who donate to qualifying scholarship organizations can receive tax credits from their state. In a handful of states, those credits are worth 100 percent of their donations, a reflection of both the high priority policymakers place on expanding educational opportunity and the potential for the state to realize savings from the scholarship program. At the same time, taxpayers can also reduce their federal taxable income by deducting their charitable contributions.

This is what the AASA and ITEP call “double-dipping,” which they define as “receiving a tax benefit on the same donation at both the federal and state level.” However, taxpayers who itemize could have deducted their state taxes from their federal tax liability instead of donating—a longstanding policy that no one would consider “double-dipping.” For that matter, according to AASA’s and ITEP’s definition, anyone who receives both a state and federal deduction for their same donation would be considered “double-dipping” – a category that includes nearly every American who makes charitable contributions in states with income taxes!

To illustrate: John Q. Taxpayer earns $100,000 and is subject to a 10 percent state income tax and a 25 percent federal income tax. (To simplify, we’re assuming flat income taxes with no other deductions, though the math of progressive income taxes is more complicated.) If he pays his state income tax of $10,000, he can then deduct that amount from his federal taxable income, so he pays the IRS 25 percent of $90,000, or $22,500. We’ll call this Option A. However, if John goes with Option B by making a $10,000 donation to a scholarship organization and taking a 100 percent credit, he will reduce his state tax liability to $0, and then he can deduct his donation from his federal taxable income. Yet again, he will pay the IRS 25 percent of $90,000, or $22,500. In each case, Johnny has exactly the same amount of money left in his pocket—the only difference is whether he gave $10,000 to his state or a scholarship organization. Calling one scenario “double-dipping” but not the other is nonsensical.

However, federal tax policy is a bit more complicated than this. Some taxpayers are subject to the Alternative Minimum Tax, which was a policy intended to make sure that wealthier tax filers did not pay below a certain minimum after their accountants applied a variety of tax benefits and deductions. This is where the AASA/ITEP’s faulty claims of “profiting” come in.

Taxpayers subject to the AMT can deduct their charitable donations from their federally taxable income, but not their state taxes. So, in the scenario above, had John been subject to the AMT, he would have had to pay $25,000 to the IRS if he paid his full $10,000 in state taxes. The difference between Option A and Option B is what AASA and ITEP call “profit.” Option B is a “profit” only if we consider Option A the base amount that should be owed – but it is equally valid to consider Option B the base amount (particularly since all other tax filers can deduct their charitable contributions from their taxable income), in which case someone going with Option A would be getting less than what they “should” in federal tax benefits. It’s all relative to what we consider the base.

Moreover, as if their definition of “profit” were not peculiar enough, calling this a “get-rich scheme” is entirely disingenuous. In order to realize a federal tax benefit beyond what they’d already receive from just paying their state taxes, donors would already have to be well-off enough to be subject to the AMT.

In the end, none of this should have any bearing on whether state lawmakers enact these policies. State treasuries are unaffected by the difference in taxpayers’ federal tax liabilities, and state policymakers have no control over federal tax policy. The feds could decide tomorrow that state taxes are deductible from the AMT or that charitable contributions are not, and there would be no more so-called “profit.”

To the extent that federal policymakers are concerned about TCS policies—or various other state tax credits, such as Arizona’s 100 percent tax credits for donations to organizations that help low-income families such as Big Brothers/Big Sisters, YMCA, United Food Bank, etc.—they could simply disallow taxpayers subject to the AMT from deducting tax-credit-eligible donations. On the other hand, they may want to keep the existing tax code in place to spur private giving. As Nobel Laureate economist Robert Shiller argued in the New York Times, such tax benefits can provide an even greater benefit to society:

We have to clear our minds of the idea that the charitable deduction is a “loophole” that benefits the rich at society’s expense. Income that is freely given away should not even be considered as taxable income.

Yes, the wealthy use this deduction more often, and give greater amounts of money. But society benefits. And beyond the money involved, the tax break for donors conveys a sort of official recognition, and encourages a habit and a culture of giving.

We don’t rely on government to set all of our goals — even our social goals, our wishes for the nation’s future. The essential question we all must answer is how we can achieve the good society.”

The Fiscal Impact of Tax-Credit Scholarships

The AASA/ITEP report also claims that TCS policies “divert over $1 billion per year toward private schools” instead of public treasuries and district schools. Setting aside that this is less than 0.16 percent of the more than $625 billion spent annually on public education nationwide, the report tells only half the story. It’s true that tax-credit scholarships reduce state revenue, but they also reduce state expenditures on K-12 education. Focusing exclusively on one side of the balance sheet is a highly misleading tactic we’re used to seeing from those who’d rather pump money into a system than have it follow individual students.

State funding of district schools is generally tied to enrollment. If a student leaves a district school for any reason—whether she accepted a tax-credit scholarship, started homeschooling transferred to another public school district, or moved out of town—the state generally no longer pays the district for that student, though in some cases, “hold harmless” provisions mean the state does pay for “ghost students” who are no longer enrolled. Moreover, regardless of enrollment, school districts keep all locally raised revenue and most federal funds.

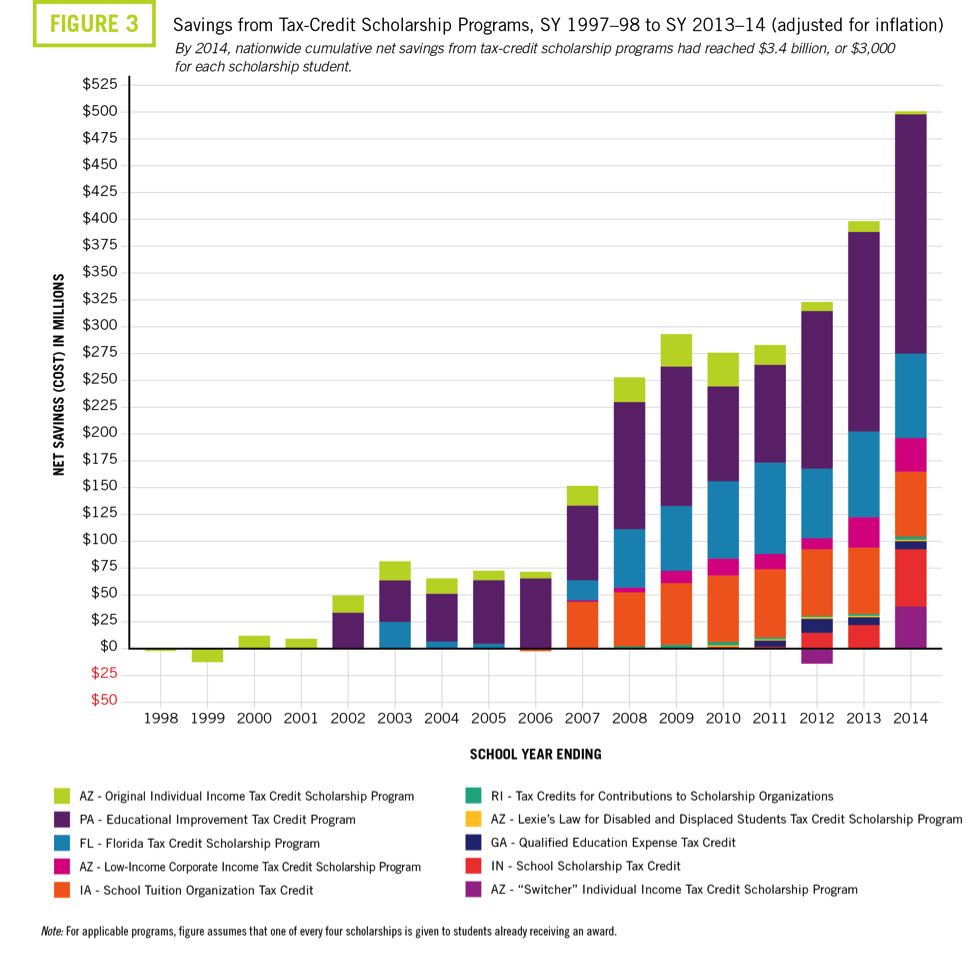

When a donor receives a tax credit, that reduces the amount of revenue the state collects. Likewise, when a student switches out of a district school to accept a tax-credit scholarship, that reduces the state’s expenditures. A 2010 report from the Florida legislature’s Office of Program Policy Analysis and Government Accountability found that for every $1 in decreased revenue, the state’s TCS policy produced $1.44 in reduced expenditures.

Florida is not unique. A recent analysis of 10 tax-credit scholarship programs by EdChoice estimated savings worth more than $580 million nationwide in FY 2014, even after accounting for students who would have enrolled in a district school anyway. From FY 1998 through FY 2014, the TCS policies produced an estimated $1.7 billion to $3.4 billion in savings, the equivalent of approximately $1,650 to $3,000 per scholarship student.

Source: Martin Lueken, “The Tax-Credit Scholarship Audit,” EdChoice, October 31, 2016.

Of course, to the extent that AASA and ITEP implicitly recognize the existence of a reduction in state expenditures, they claim the TCS policies “drain” funds from district schools. The unstated assumption is that those funds—and therefore the children to whom they are attached—were somehow owed to the district schools. Parents are unlikely to agree. State constitutions impose a duty on states to ensure that its young citizens have access to an education, but those students do not have a duty to attend assigned schools. Indeed, policymakers are increasingly seeing the wisdom in having state funding follow a child to the school of their family’s choosing.

Moreover, it is worth repeating that TCS policies only affect state funds, not local or federal funds. This is important because schools face both fixed and variable costs. Although some school choice opponents would have the public believe that nearly all district school costs are fixed, Dr. Ben Scafidi has estimated that, on average, only approximately 36 percent of district school costs are fixed. Indeed, if it were true that most or all school costs are fixed, then there would be little need to fund enrollment growth—but we know that’s not the case. Rather, nearly two-thirds of the typical district school’s costs change with student enrollment. This means that even where TCS policies might reduce state funding for some district schools, most schools are unlikely to notice a significant difference.

Finally, it should be noted that state policymakers have broad discretion in how they use the savings from TCS programs. They could lower taxes, pay down state debt or invest the savings in district schools or other student services.

Contrary to the claims of the AASA and ITEP, tax-credit scholarship policies neither enrich donors nor drain the public coffers. Such frivolous charges are intended to distract from what TCS policies actually do: provide taxpayers with an incentive to help low- and middle-income families choose schools that work for their kids. They are the true beneficiaries of TCS programs, and expanding educational opportunity should always be considered a worthy public policy goal.

–Jason Bedrick and Marty Lueken

Jason Bedrick is Director of Policy at EdChoice. Martin Lueken, Ph.D., is Director of Fiscal Policy and Analysis at EdChoice.